Ten factors affecting the dollar

2023-10-03

BY CHELTON WEALTH

Asking the question “What do you think of the dollar?” is relatively straightforward. The answer, however, is not. One answer that is always correct is that the dollar is likely to remain the US currency for years to come, but this is probably not the answer to the question. Incidentally, the same answer is much less definite with the euro.

Predicting the dollar is not easy. There are 10 factors that affect the dollar. These can still be identified. The problem lies in the weight to be assigned to those factors. Currency markets are often manically monogamous. Usually, strong emphasis is placed on one specific factor and the others seem to play no role until they do.

Below is an overview of the 10 factors that affect the dollar:

1, Top-down, a strong economy also includes a strong currency. In that respect, it is explicable that the dollar is stronger than the euro, for example. Especially now that the euro has slipped towards a stagflationary scenario in recent months while the US economy seems to be making a perfect landing, this helps the dollar. In the long run, economic growth is more of an argument as to why the dollar will eventually lose out to, say, the renminbi.

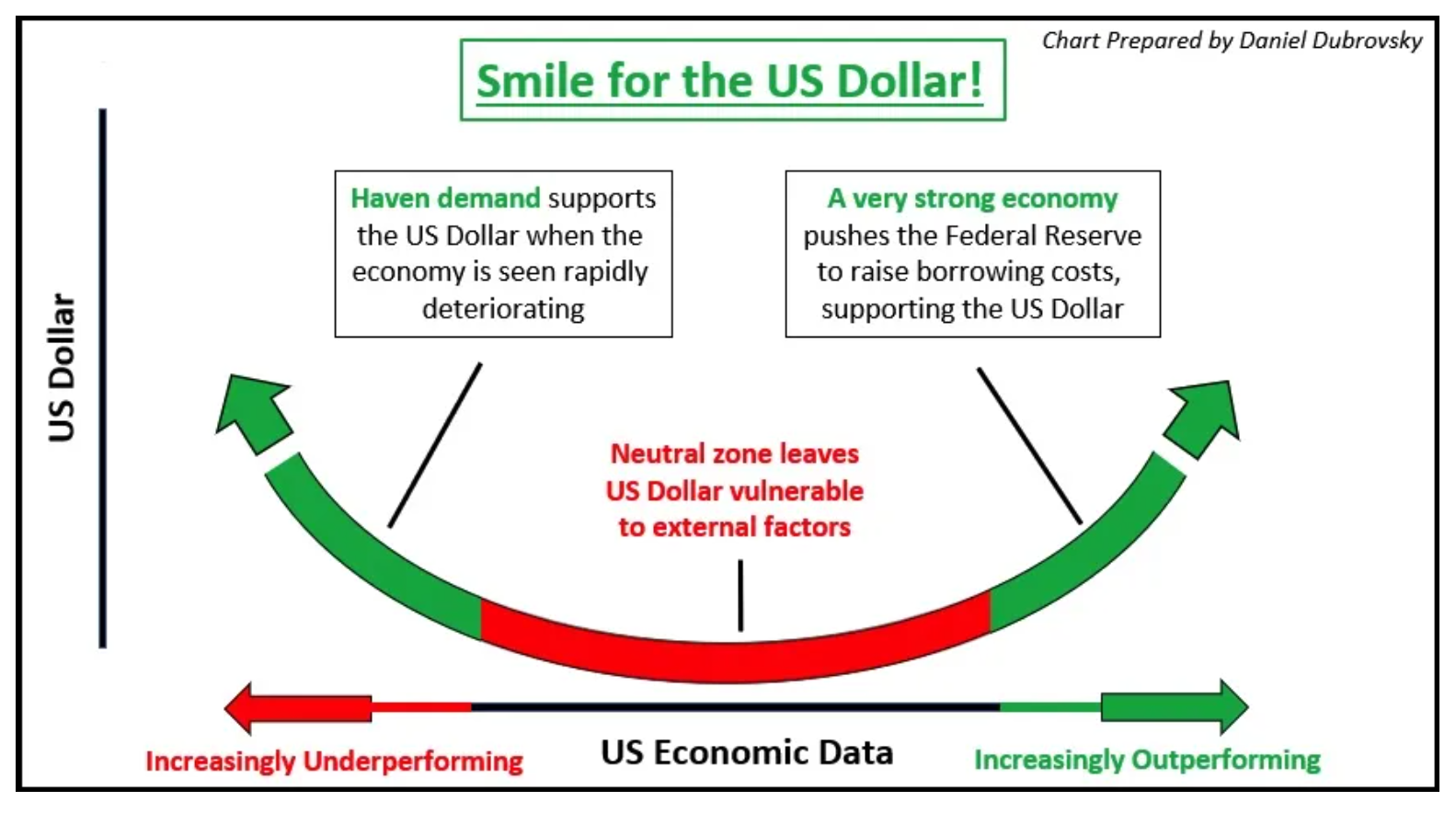

2. The dollar is a special currency. It is still the world’s reserve currency. As a reserve currency, the United States is effectively a banker to the rest of the world. This makes it possible and even desirable to constantly run a current accountdeficit. Because of that deficit, the reserve currency looks fundamentally weak but is actually relatively strong. A well-known example in this context is the chart of the dollar smile, a chart where the dollar is strong precisely when there is a crisis (everyone flees the dollar) or at the other extreme when the US economy is doing very well. In both cases, the dollar is rising. Only in between, does the dollar tend to fall because that is when fundamentals come to the surface.

3. Interest rate differentials can have a big impact. If you want to arbitrage currencies, you naturally receive interest in the currency you are long and pay interest in the currency you are short. For instance, the proverbial Ms. Watanabe borrowed for years in yen which she put out in other dollars. Only this kite no longer holds true due to recent developments (inflation) in Japan.

4. Monetary policy. At a time when the Fed is hitting the brakes full on and other central banks are still easing quantitatively, this is good for the dollar. This is not just a matter of interest rate differentials, but mainly of how future monetary policy will deviate from the policy the market is currently reckoning with.

5. Geopolitical relationships. The UnitedStates has used the dollar as a weapon against the Russians. The Russians have no use for dollars because they can no longer pay with them through the financial system (Swift). After all, their accounts are blocked. Other countries that sometimes also have (or may have in the future) a difficult relationship are taking this into account. Rich Arabs and Chinese billionaires are therefore better off not holding dollars. Before you know it, they will be in the same boat as the Russian oligarchs. Furthermore, one should also not underestimate the negative effect of polarisation within US politics in this context. That does not help the dollar.

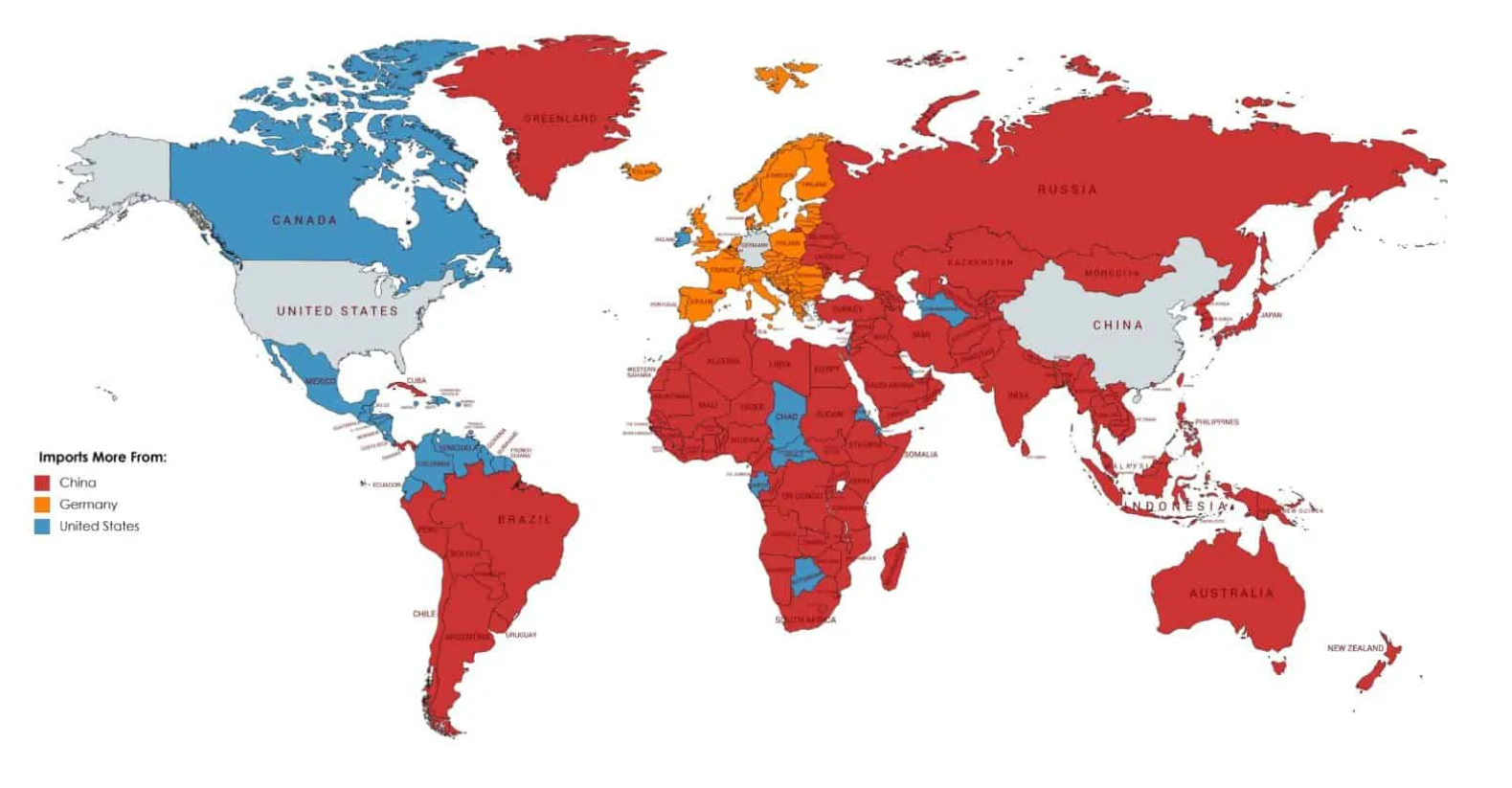

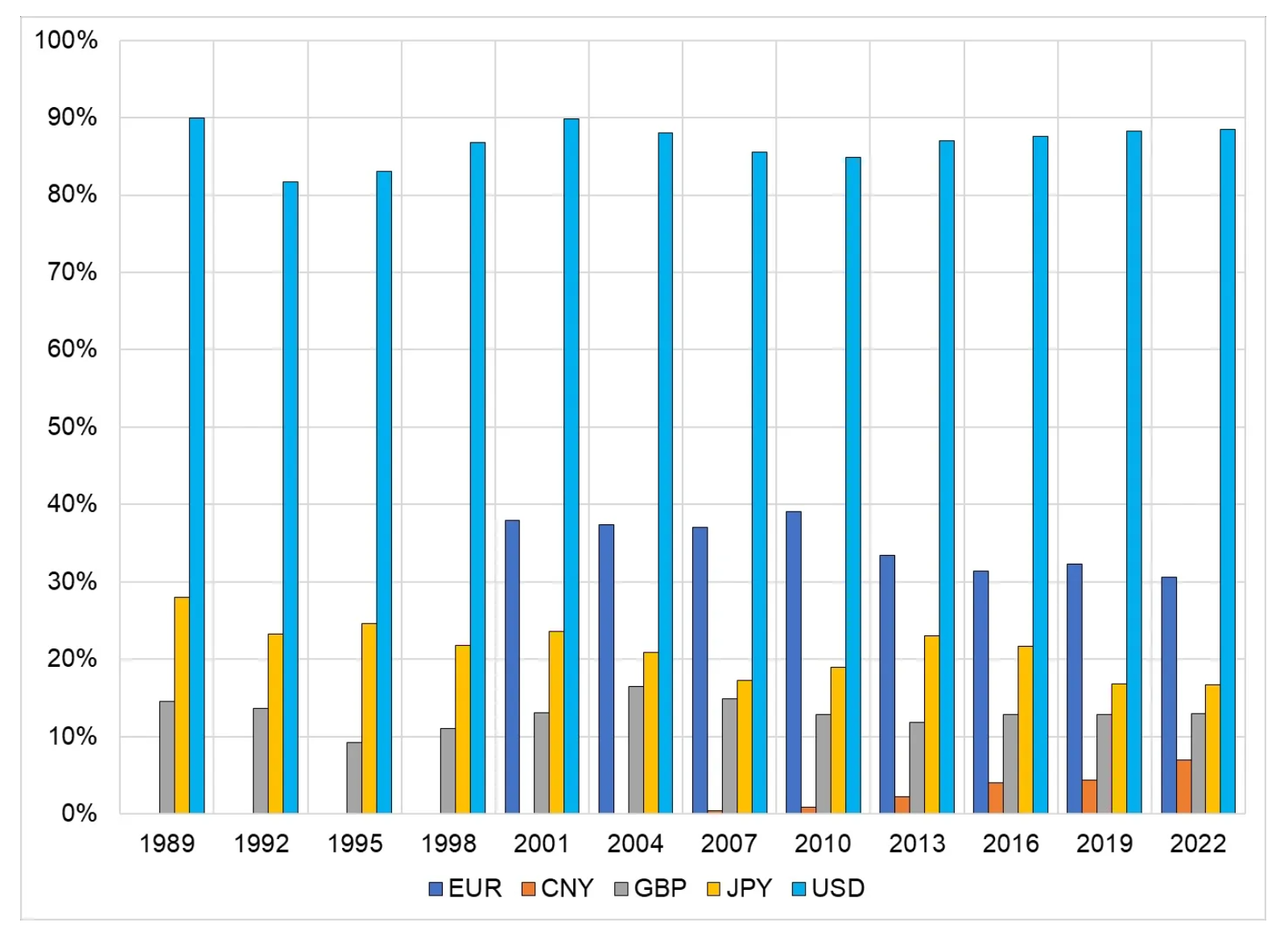

6. Dollarization. Since the Great Financial Crisis, the Chinese have wanted to get rid of their dependence on the dollar. This was not even so much because of a deteriorating relationship with the US, but mainly because the Chinese economy was too dependent on the dollar and thus US banks. Actually, Asian countries have been trying to reduce their dependence on the dollar since the 1997 Asia crisis. Incidentally, saying goodbye to the reserve currency is not that easy. It is not like Microsoft’s operating system. It is not the best operating system, but because everyone uses it, it is hard to get out of it. Incidentally, in recent times you see rather a de-euroisation, which of course is also linked to European sanctions against the Russians, which has reduced the euro’s appeal for wealthy people outside the eurozone. Gradually, the euro’s share in world trade is declining and the renminbi’s share is rising. However, the dollar remains by far the most important currency.

7. Twin deficits. Countries with constant budgets and current account deficits have weak currencies, only this apparently does not apply to the dollar. The risk, however, is that if the dollar loses its reserve status, things could quickly go the other way too. By running deficits, the rest of the world is actually financing US deficits and the US economy. This is the privilege of the residual currency. The United States is home to 5 per cent of the world’s population, but its share of current account deficits is 60 per cent. Furthermore, 40 per cent of the US budget deficit is structurally financed by foreign countries.

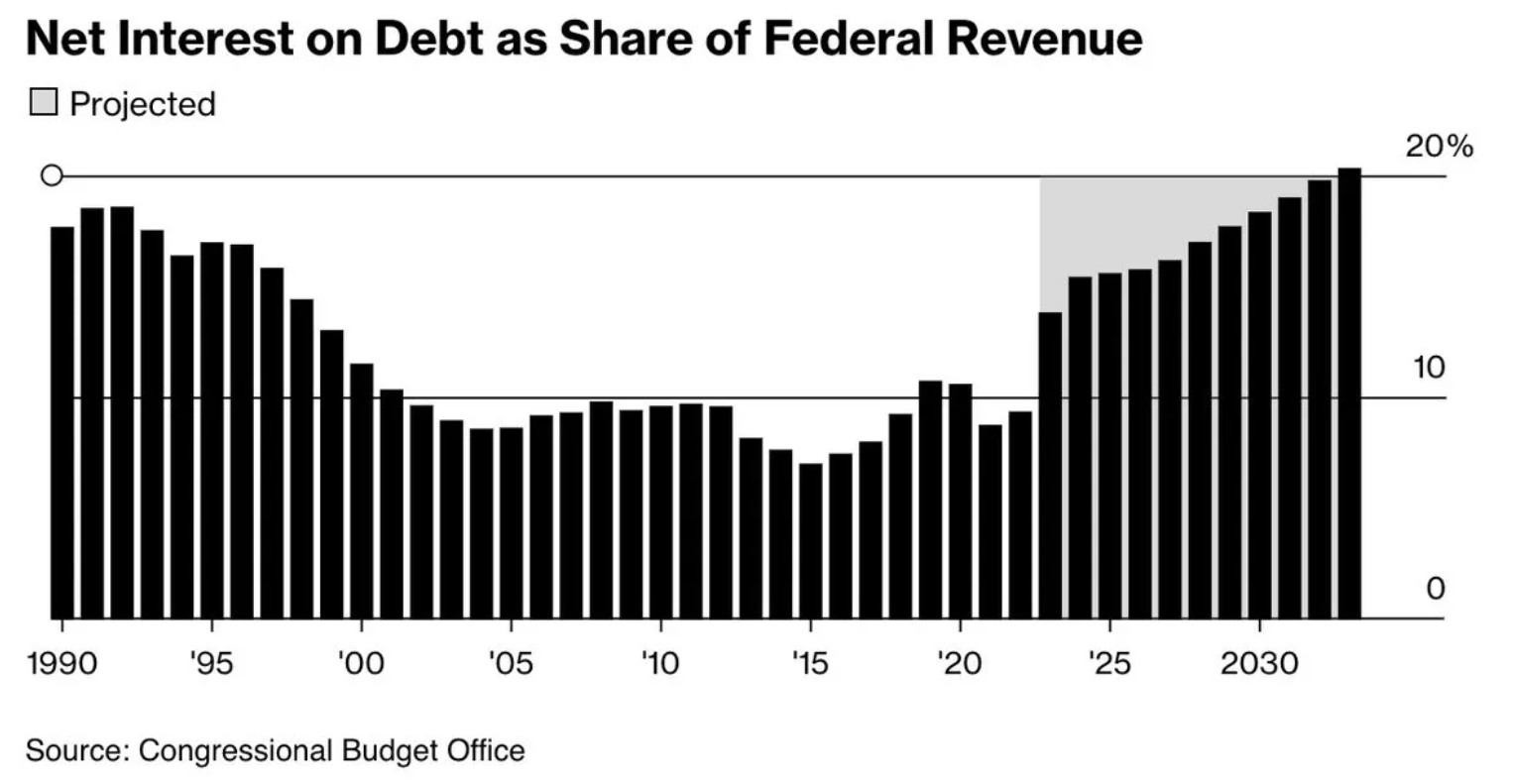

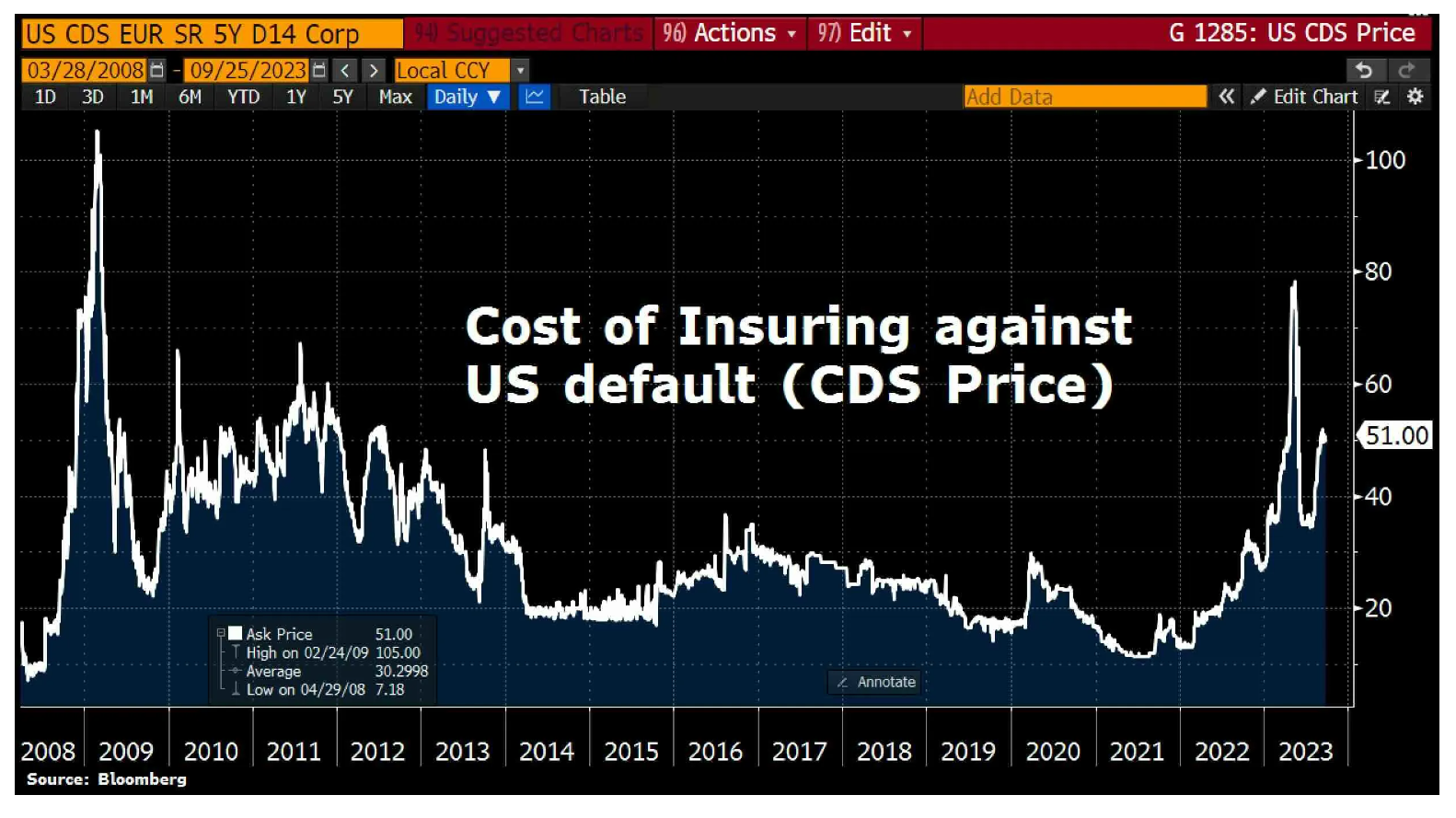

8. Debt. Countries with high debts (to foreign countries) can always repay their debts, provided they have their own currency. The big question, though, is what then is the value of the currency? The mechanism of financial repression and reflation ensures that the nominal economy grows more than the nominal debt, often through more inflation. The US national debt has recently surpassed trillion. The US government may soon have to shut down under the credit ceiling. Furthermore, credit rating agencies S&P and Fitch have downgraded the US from AAA to AA, but in a world where there is a glaring shortage of risk-free paper, US Treasuries continue to fill this role for now.

9. Money flows. Many factors are more fundamental in nature, but ultimately money flows determine currency strength. A good example is the year 2001. Back then, pretty much all the above factors would argue for a weak dollar, but because the renminbi was pegged to the dollar at the time, a lot of money flowed into the dollar-renminbi bloc (thanks to China joining the WTO). This could also happen, for instance, when oil prices are high (oil is still largely traded in dollars). As for that high oil price, Europe has to buy energy in dollars these days (it was mostly in euros until recently) and, of course, Europe has to earn those dollars first.

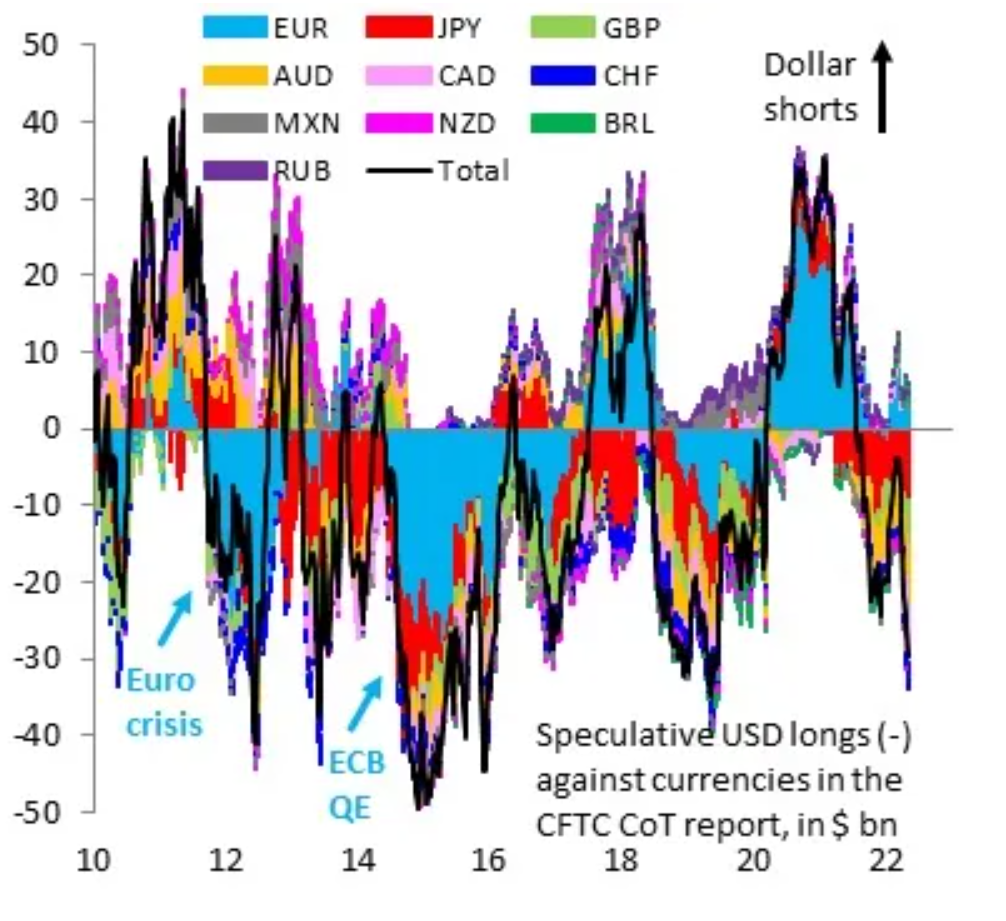

10. Positioning. Besides money flows and fundamentals, everything can go haywire if there is extreme positioning. If the market bets fully on a weakening dollar, you are more likely to see a stronger dollar in the shorter term. This is because basically all other factors are already factored into the price of the dollar and if everyone is negative, the only possibility is that someone is going to become more positive, causing the dollar to rise.

To estimate the development of the dollar, it is important to know how the market views these 10 factors and estimate in which the own scenario differs from the market scenario. Europeans tend quite often to underestimate the strength of the dollar, but in the somewhat longer term, it seems justifiable to forecast a weaker dollar, especially against Asian currencies. The near-term trigger for this could be a mild recession in the US next year, although, for instance, the US government shutdown due to the credit ceiling and the US presidential election next year will also be a trigger for a weaker dollar.