The Japanese Yen in 2024

2023-12-12

BY CHELTON WEALTH

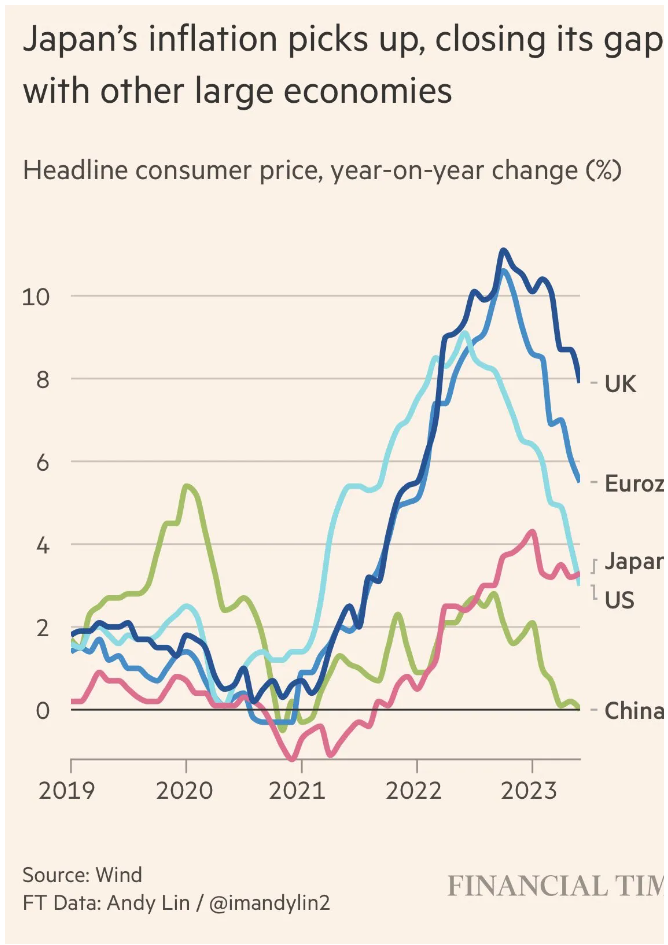

The yen reached its highest point in three months versus the dollar last week after Governor Kazuo Ueda signalled that the Bank of Japan is nearing the end of its ultra-loose monetary policy. On 19 December, the Bank of Japan will make another decision on that policy. The probability of an interest rate hike has risen sharply in a short time when, in fact, the market has been waiting for it for more than a year. The Yield Curve Control (YCC) policy originally intended to support banks by ensuring a steep yield curve has degenerated into a procyclical policy that conflicts with efforts to strengthen the yen. At a time when the Japanese economy is doing badly, YCC is putting an extra brake on the economy due to the need to keep long-term interest rates high. At the moment, things are going well, and inflation is picking up. YCC provides another extra boost by buying up bonds.

GRADUAL DEPARTURE OF YCC

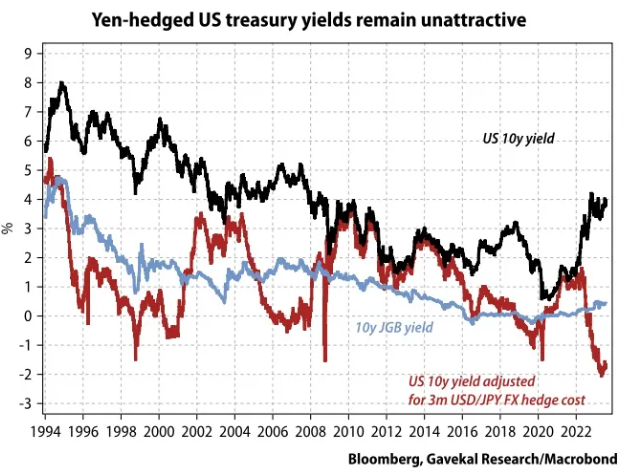

It did become clear last year that Japan is also opting for a gradual transition in monetary policy under Ueda. Other central banks take much bigger steps at the time of policy reversal. This has sharply increased the contrast with monetary policy in Europe and the United States in recent years, further weakening the yen. The need to stop the YCC policy is also evidenced by the fact that Japanese inflation has reached its highest point in 40 years. If the YCC policy is abolished, interest rates in Japan could rise, although there is still a significant savings surplus. A surplus is also rising sharply due to the repatriation of foreign investment, and a current account surplus is near its highest point ever. However, the gap between US and Japanese interest rates has narrowed rapidly since the 10-year peak at 5 per centin late October.

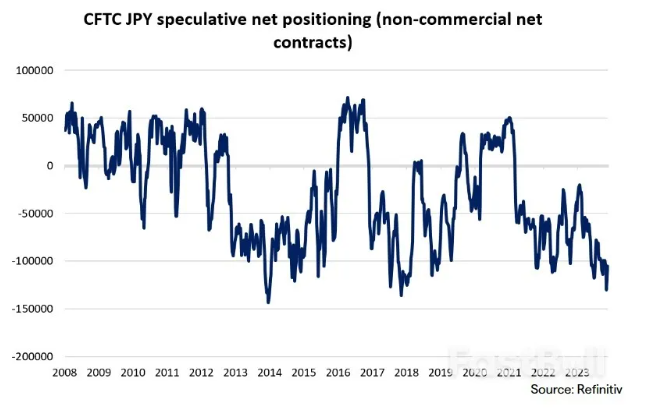

THE MARKET IS MASSIVELY SHORT ON THE YEN

The market is still massively short on the yen. The interest rate differential between Japan and the rest of the world is still being exploited to the full. If the yen also weakens, this could be lucrative in the short term. With the Japanese yen not being this cheap in 50 years, the likelihood of this turning soon increases. Then, the Japanese central bank will start tightening, while other central banks may start easing due to rapidly falling inflation. Then, the yen could quickly gain strength, partly by hedging short positions.

TARGET REACHED

Meanwhile, inflation is getting into the minds of more and more Japanese. In this respect, the Bank of Japan has reached its target. Whereas inflation initially rose thanks to rising energy prices and a weak yen, wages are now also rising. At the same time, Japanese living on nominal pensions are starting to squeak. These have benefited for years from an environment where prices remained flat or even fell but are now seeing the cost of living rise. Japanese households hold as much as half (a total of trillion) of their assets in cash and short-term deposits. These must look for a better-yielding asset within Japan (equities?). The government does help them with a package of measures with an equivalent value of 3 per cent of GDP. This additional demand will also create more inflation.

COMPETITIVENESS

Japan is still an industrial powerhouse, and the yen being so extremely undervalued has long-term implications for competitive relations. The cheap yen allows Japan to compete well with China and South Korea, but it is clear that the German industry is starting to lose market share to Japan (and China). Moreover, it is mainly the weak yen causing inflation in Japan. This is not the first time Japan’s competitors have started complaining about unfair competition and demanding action. This can be prevented by a stronger yen, for instance, through the Bank of Japan’s tightening policy, preferably combined with the looser policies of central banks outside Japan.

A STRONGER YEN

There are several reasons why the yen may gain strength next year. Because everything is so cheap in Japan, interest from foreign investors is also increasing. This should be noticeable next year in the number of tourists visiting the country. Only in May this year did the requirement for face masks expire in large parts of public transport. Furthermore, China is keen to deal with its ‘too’ large dollar position. Given the economic ties between China and Japan, China can exploit the weak yen by swapping US dollar positions for Japanese assets. Good news for Japanese assets. For the Nikkei, it is still just over 20 per cent to its all-time high from 1989.