The Mar-a-lago Accord

2025-03-14

BY CHELTON WEALTH

The Mar-a-lago Accord

The summer palms of Mar-a-Lago sway in the gentle breeze while a new chapter in global financial history may be written in the stately halls of this ‘Southern White House’. Forty years after the famous Plaza Accord, in which the dollar was devalued to stimulate American industry, Donald Trump seems determined to implement a similar, but perhaps even more radical restructuring: the Mar-a-Lago Accord. The speculation about this agreement is nothing new. Financial experts were already whispering about the possibility during the election campaign. In the summer of 2024, Scott Bessent — still the intended finance minister of the United States — openly speculated with Bloomberg about such an agreement. With Trump’s return to the White House, these plans seem to be taking shape. But what exactly does this agreement entail, and why could it be more important than many think?

More than just a weaker dollar

The Mar-a-Lago Agreement is not simply a plan to devalue the dollar. It is a comprehensive strategy to fundamentally reshape the global financial structure. Stephen Miran, Trump’s choice for chairman of the Council of Economic Advisers, has developed this vision.

Team Trump wants to ‘encourage’ other countries to convert their assets into dollars, short-term government bonds, or even gold into long-term or perpetual dollar bonds. These bonds would be suitable for repo agreements with the Federal Reserve. The goal is to reduce the fiscal pressure on the US while maintaining the dominance of the dollar system, while Washington can weaken the currency.

A radically different philosophy

For many mainstream economists, this plan seems crazy. It goes against years of economic orthodoxy. However, we must understand that Trump’s team is pursuing a radically different philosophy. They do not see financial interventions as obsolete but essential for a large-scale global trade and finance reorganisation. Where traditional economists fear stock market crashes and recessions, Trump’s team sees opportunities. They have always known that tariffs will initially cause economic pain, but want to endure this early in Trump’s term. What’s more, they see advantages: a recession would force other countries to the negotiating table more quickly, lowering American interest rates and counteracting the excessive financialisation of the American economy.

Trump’s ‘colour scheme’

An intriguing aspect of Trump’s plan is his ‘colour scheme’. Trump’s finance minister Scott Bessent has said that Trump will ask other governments to place themselves in ‘red’, ‘green’ and ‘yellow’ categories — enemies, friends or neighbouring players. ‘Green’ countries will receive military protection and tariff relief, but must embrace a currency agreement. Some ‘yellow’ — or even ‘red’ — countries could conclude transactional deals. This suggests a phased approach to the Mar-a-Lago Agreement: first, a phase with allies, and then one with others. It is a form of economic diplomacy we have not seen in recent decades.

The dollar paradox

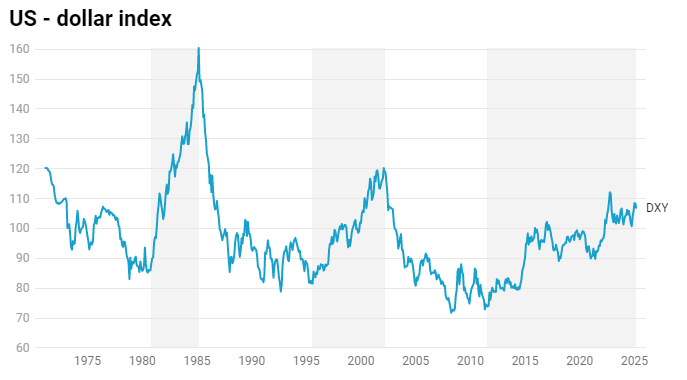

Trump’s team faces an interesting paradox: while they want to weaken the dollar to stimulate American industry, they also want to maintain dominance in the global financial system. Scott Bessent has explicitly stated this: weakening the dollar and maintaining its dominance are not ‘mutually exclusive’ goals. This approach comes when the dollar’s dominance is already under pressure. The peak in dollar reserves worldwide was reached in the early seventies at 85 percent, but has since fallen to 57 percent. Using the dollar against countries like Russia has also led other countries, such as China, to reduce their dollar holdings.

Chance of success?

Realising a Mar-a-Lago Agreement is no easy task. The dollar has risen since Trump’s re-election. Moreover, international cooperation is not precisely one of Trump’s strong points. What he is good at, however, is exerting pressure. One of the components of the Miran plan is to convert foreign positions in American government bonds into very long-term (100-year) zero-coupon bonds. This could succeed under the pressure of sufficient import tariffs. The coming quarters will therefore be crucial for the chance of a Mar-a-Lago Agreement.

The new Bretton Woods?

Bessent stated last year that he ‘wants to be part of … Bretton Woods restructurings’ for the global financial and trade system. This was no joke. The current tariff shocks could be a harbinger of a much bigger drama. Whether the Mar-a-Lago Agreement will succeed is uncertain. Many mainstream economists will argue that these plans are so wrong that they will fail. However, investors need to understand that Trump’s recent actions are not ‘just’ erratic; his team’s vision has a robust internal logic. The current chaos is as much a feature as it is a flaw. It is chaos with a purpose. As we approach the 40th anniversary of the Plaza Accord, we will prepare well for a possible new chapter in global economic history. A chapter that may well be written in the shadow of the palms of Mar-a-Lago.